Note: The information on this page may not be updated. For latest updates, click here.

Goods and Services Tax (GST) was launched in July’17 to unify the numerous indirect taxes. All the business entities are required to complete GST Registration and file their GST return forms online or offline.

UPDATE: As a part of the COVID-19 relief package announced on 13th May’20, the last date to file GST returns has been extended to the end of June, 2020.

New GST return system to be introduced from April, 2020 (earlier proposed from October, 2019) as per the 37th GST Council Meeting.

Table of Contents :

What is GST Return Form?

GST Return Form is a document containing details of all purchases, sales, output GST (on sales) and input tax credit (GST paid on purchases) to calculate an assessee’s GST liability for a particular tax period. Currently GST returns can be filed either on monthly, quarterly or annually depending on various applicable factors.

Who should file GST Return?

All business dealers and owners who have registered under the GST system are required to file their GST returns using applicable forms either online or offline.

Generally, a regular business has to file 2 monthly returns (GSTR-1 & GSTR-3B) and 1 annual return (GSTR-9), thereby making a total of 25 GST returns in a year.

Please note that composition dealers are required to file GST via different forms.

Types of GST Returns and their Due Dates

| Type | Purpose | Frequency and Due Date |

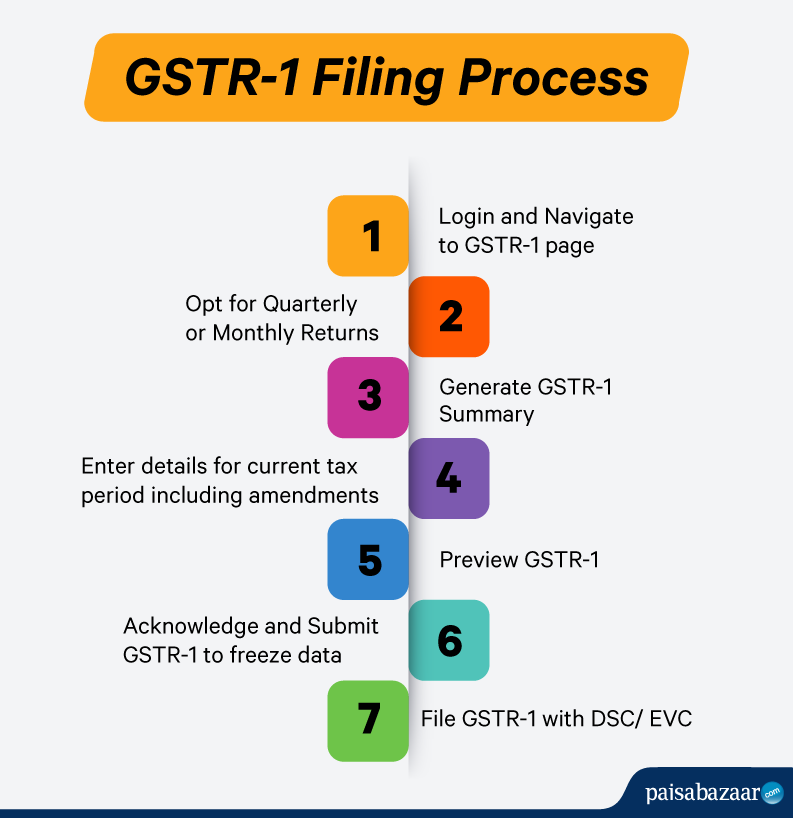

| GSTR-1 | To be filed by all the normal taxpayers stating their outward supplies of goods and services during the applicable tax period. | Turnover < Rs. 1.5 crore – Quarterly, 31st of the month succeeding the quarter

Turnover > Rs. 1.5 crore – Monthly, 11th of the succeeding month |

| GSTR-2

Suspended |

Details of inward supplies of goods and services including those under reverse charge basis | Monthly, 15th of the succeeding month |

| GSTR-3

Suspended |

All details of the outward and inward supplies, as mentioned in Forms GSTR-1 & GSTR-2 | Monthly, 20th of the succeeding month |

| GSTR-3B | To be filed by all the normal taxpayers declaring their summary GST liabilities for the applicable tax period | Monthly, 20th of the succeeding month |

| CMP-08

(Earlier GSTR-4, for composition-scheme taxpayers only) |

To declare summary of outward supplies and import of services liable to reverse charge mechanism | Quarterly, 18th of the month succeeding the quarter |

| GSTR-5

(for non-resident taxpayers) |

To be filed by non-resident taxpayers when they do not wish to claim Input Tax Credit (ITC) | Monthly, 20th of the succeeding month |

| GSTR-5A | To be filed by Online Information and Database Access or Retrieval (OIDAR) service providers outside India for their services to unregistered persons in India | Monthly, 20th of the succeeding month |

| GSTR-6 | To be filed by Input Service Distributors for distribution of ITC

|

Monthly, 13th of the succeeding month |

| GSTR-7 | To declare TDS liability by the authorities deducting tax at source

|

Monthly, 10th of the succeeding month |

| GSTR-8 | To declare Tax Collected at Source (TCS) by e-commerce operators | Monthly, 10th of the succeeding month |

| GSTR-9 | To be filed by all the normal taxpayer declaring the details of purchase, sales, input tax credit, refund claimed, demand created, etc. | Annually, 30th November’19 for FY 2017-18 |

| GSTR-9A | To be filed by GST composition scheme taxpayers declaring the details of outward supply, inward supply, taxes paid, refund claimed, demand created, input tax credit and reverse due to opting out or opting in to the composition scheme. | Annually, 30th November’19 for FY 2017-18 |

| GSTR-10

(Final Return) |

To be filed by the taxpayers, whose GST registration has been canceled or surrendered to file final GST returns. | Once, 3 months from the date of cancellation or order of cancellation, whichever is later |

| GSTR-11 | To be filed by Unique Identity Number (UIN) holders stating the supplied/received goods and services.

To claim GST refund through RFD-10

|

Quarterly, not mandatory for UIN holders who did not receive any inward supplies during the quarter.

28th of the next month for which refund statement is filed |

Note: The GST return due dates may be extended by the Government from time to time.

Check out GST Calendar for more details about the filing deadline dates of various GST return forms.

Get FREE Credit Report from Multiple Credit Bureaus Check Now

Penalty for Late Filing of GST Return

Filing GST return is mandatory for all the GST registered dealers and business, including those with nil returns. Any delay in filing of GST return will lead to implementation of both late filing fees and penal interest.

Late Filing Fees for Intra-state Dealings

| Applicable GST Act | Late filing fee/day |

| Central Goods and Services Act, 2017 | Rs. 100 |

| State Goods and Services Act, 2017 or Union Territory Goods and Services Act, 2017 | Rs. 100 |

| Total | Rs. 200 |

NOTE: The maximum late filing fees for each monthly/quarterly filing as per each GST Act cannot be more than Rs. 5000. While the maximum amount chargeable as late filing fee for each annual GST return (GSTR 9) cannot be more than 0.25% of the turnover.

Late Filing Fees for Inter-state Dealings

As per the Integrated Goods and Services (IGST) Act, the penalty for late filing of IGST returns is equal to the sum of the penalties as per CGST Act and SGST/UTGST Act.

Thus, late filing of IGST will lead to a fine of Rs. 200/day. Please note that the maximum late filing fee for monthly/quarterly IGST return cannot be more than Rs. 10,000 for each filing. While the maximum amount of late filing fee for each annual GST return (GSTR 9) cannot be more than 0.25% of the turnover.

NOTE: The late filing fees are subject to change as per CBIC notifications.

UPDATE: CBIC has reduced the late filing fees for delayed filing of GSTR 1*, GSTR 3B, GSTR 4, GSTR 5 and GSTR 6 as follows:

For Intra-state dealings

| Act | Reduced late filing fee/day |

| CGST | Rs. 50 |

| SGST | Rs. 50 |

| Total | Rs. 100 |

*The detailed notification with respect to late filing fees of GSTR-1 can be read here.

For Inter-state dealings

| Act | Reduced late filing fee/day |

| IGST | Rs. 100 |

For Nil Return Filers

| Act | Reduced late filing fees/day |

| CGST | Rs. 10 |

| SGST | Rs. 10 |

| IGST | Rs. 20 |

Interest on Outstanding Tax

An interest at the rate of 18% per annum will be charged on the outstanding tax in case of delayed GSTR filing. Please note that this interest is calculated from the next day of the due date.

Moreover, an interest has to be paid when a taxpayer claims excess Input Tax Credit (ITC) or reduce output tax liability in excess at the rate of 24% per annum.

Thus, GST returns should be filed well within the due dates to avoid any penalty and interest. To avoid any delay, refer to the important GST dates and the GST filing procedure.